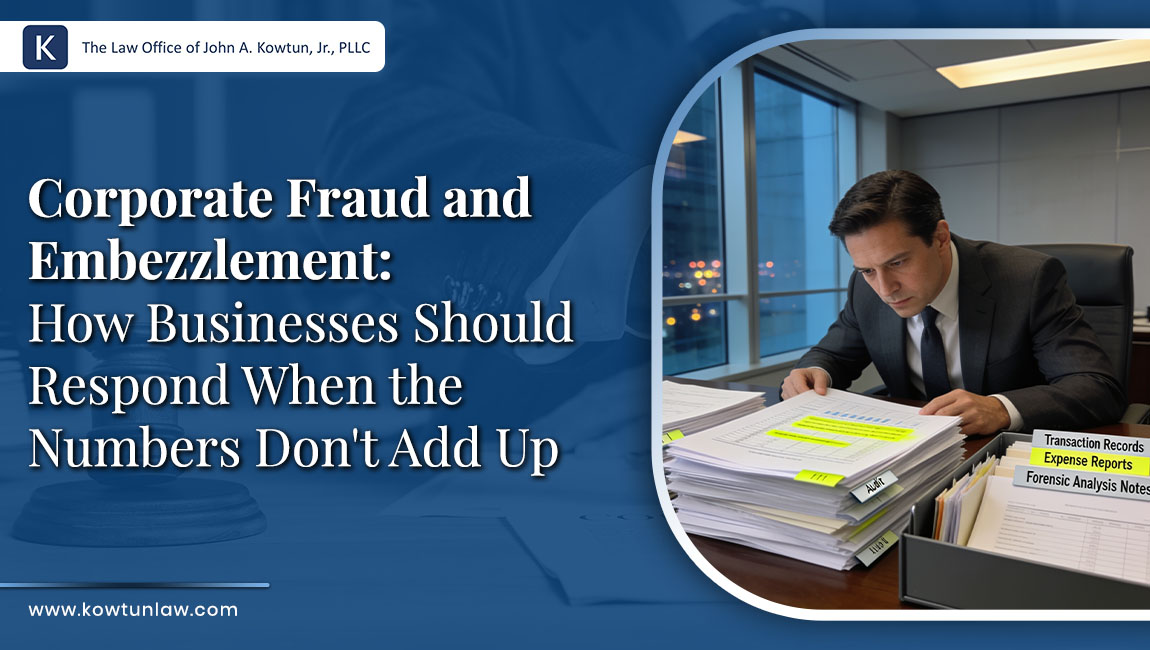

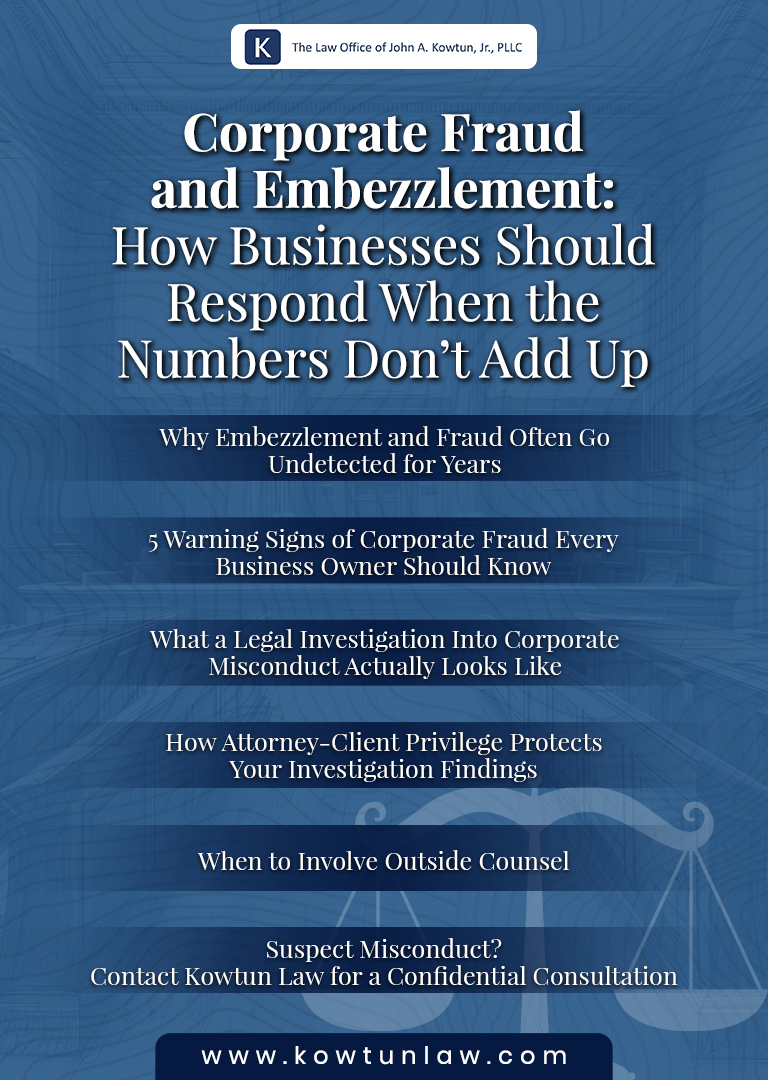

Corporate Fraud and Embezzlement: How Businesses Should Respond When the Numbers Don’t Add Up

A business owner reviews a month-end report after close and sees numbers that do not fit the usual pattern. Expenses are higher than expected, one vendor payment looks odd, and a trusted employee has an answer ready for each line item. Nothing is dramatic on its face. That is exactly why the owner hesitates to raise it, freeze access, or wait one more week.

Fraud concerns become harder to contain when a business ignores early signs, confronts the wrong person too soon, or treats a control problem like a bookkeeping mistake. The real stakes include missing funds, damaged records, employee claims, insurance issues, and a weaker position if the matter later turns into litigation. When the facts point to possible misconduct rather than ordinary error, a corporate fraud investigation attorney Texas businesses trust can help assess the records, preserve evidence, and decide on a quieter response before the company shows its hand.

Why Embezzlement and Fraud Often Go Undetected for Years

Fraud and embezzlement often stay hidden because they do not begin with a dramatic event. They start with small acts that look ordinary on the surface. A reimbursement seems routine. A vendor invoice gets approved without much review. A transfer is coded under a familiar category. When the same person controls too much of the process, the pattern can continue without much resistance.

That is also why long-running misconduct is not always a sign that ownership was careless. In many businesses, trust develops around the employee who knows the books, handles the vendor relationships, or keeps daily operations moving. Once that person becomes the default gatekeeper, fewer people ask hard questions. Reviews become lighter. Documentation becomes less consistent. By the time the numbers start raising concern, the issue may have already escalated out of control.

5 Warning Signs of Corporate Fraud Every Business Owner Should Know

Most fraud problems leave clues before anyone can prove exactly what happened. The difficulty is that those clues often look harmless when viewed one at a time. A delayed report may seem like a staffing issue. A missing receipt may seem minor. One vendor anomaly may not stand out. Trouble starts when these issues repeat, cluster around the same people, or appear alongside resistance to review. A business that watches for patterns early is usually in a better position than one that waits for a full financial crisis before acting.

- Missing or Altered Records: Financial files, receipts, or approval trails are incomplete or keep changing after questions are raised — when the paper trail breaks down, the business may lose the evidence needed to understand the loss and respond cleanly.

- Unusual Vendor Activity: Payments go to unfamiliar vendors, duplicate accounts, or vendors with weak documentation — if those transactions continue unchecked, money can leave the business through channels that were never properly verified.

- Lifestyle Changes That Do Not Match Compensation: An employee with ordinary pay suddenly shows signs of spending far beyond that income — while not proof by itself, that mismatch can point to misuse of company funds that deserves closer review.

- Resistance to Oversight: One employee avoids vacations, blocks access, or becomes defensive when records are reviewed — when one person controls too much without backup, the business may be depending on the same person who is hiding the problem.

- Recurring Accounting Irregularities: Reversals, write-offs, unexplained adjustments, or repeated exceptions appear in the same areas — if those entries are not tested early, small discrepancies can turn into sustained financial loss.

These signs do not always prove fraud, but they often justify a more disciplined review before assumptions harden into mistakes. That is also where a corporate fraud investigation attorney Texas business owners rely on can help separate patterns worth acting on from coincidences worth monitoring.

What a Legal Investigation Into Corporate Misconduct Actually Looks Like

A legal investigation into suspected fraud is more structured than a routine internal review. It is not just a meeting with the employee in question and it is not just a deeper spreadsheet check. The process usually begins with scoping the issue, identifying the records that matter, preserving relevant data, and deciding who should know about the concern at that stage. A business that reaches the point of needing a corporate misconduct attorney is often dealing with a problem that affects money, trust, and future legal exposure at the same time.

- Scope Definition: The investigation starts by identifying the suspected conduct, time period, and key systems involved — without a clear scope, the review can wander and miss the transactions that actually matter.

- Evidence Preservation: Emails, accounting records, device data, approvals, and access logs are preserved early — if that step comes too late, important records may be lost, changed, or harder to trust.

- Witness Interviews: Relevant employees, supervisors, and third parties are interviewed in a controlled sequence — poor interview order can shape stories, alert the wrong person, and make later findings less reliable.

- Document Testing: Transactions, approvals, vendor records, and supporting materials are tested against each other — if the documents are not compared carefully, the business may mistake weak controls for innocent error or miss misconduct hiding alongside normal business activity.

- Findings Assessment: The facts are organized to show what is supported, what is unclear, and what needs follow-up — if the conclusions are rushed, the business may act on suspicion rather than evidence.

- Response Planning: Management then considers discipline, recovery, reporting duties, and next steps based on a stronger record — without a measured response, the company can create new legal problems while trying to solve the old one.

A good investigation is not only about proving misconduct. It is also about helping the business respond in a way that holds together after the first urgent decision is made.

How Attorney-Client Privilege Protects Your Investigation Findings

Attorney-client privilege, which protects certain communications made for legal advice, can be an important part of a fraud investigation when the process is designed carefully. Businesses often assume privilege exists automatically if a lawyer is copied on messages or reviews the file later. That is not always correct. The protection usually depends on why the communication was made, who received it, and how the investigation was structured from the start.

- Legal Advice Purpose: Privilege is strongest when the communication exists to seek or give legal advice — if the purpose looks mostly operational, the business may later have to produce records it thought would stay private.

- Counsel-Directed Process: Investigations directed by counsel are often easier to defend on privilege questions — without that structure, sensitive findings may be treated like ordinary business documents.

- Controlled Distribution: Investigation notes and updates should be shared only with people who truly need them — once sensitive material circulates widely, the claim of confidentiality becomes harder to maintain.

- Careful Written Summaries: Drafts, notes, and findings should be prepared with discipline — loose wording can create documents that damage the business even if the core investigation was sound.

- Separate Legal and HR Functions: Legal advice should not be blended casually with routine personnel administration — when those functions mix too freely, the business may weaken the protection it expected to have.

- Planned Final Reporting: The form and audience of the final report should be considered before anything is issued — a poorly framed report can become the document that defines the dispute later.

Privilege can protect part of the process, but it works best when the investigation itself is thoughtful and controlled from the beginning.

When to Involve Outside Counsel

Outside counsel is often worth considering before the business confronts the suspected employee, widens the conversation internally, or makes a quick disciplinary move. Timing matters because the first internal response often shapes everything that follows. A direct accusation may alert the wrong person. A rushed suspension may affect access to records before they are preserved. An informal conversation may create statements that complicate later interviews. When the concern involves money, false records, executive involvement, or a gatekeeper employee with unusual system control, the safest first step is often a quiet conversation with outside legal service providers before anyone inside the company is alerted.

That does not mean every accounting irregularity requires a formal outside investigation. Some problems do turn out to be error, weak training, or ordinary internal sloppiness. The point is to know the difference before the company shows its hand. An investigative attorney can help the business decide whether the issue is isolated or systemic, whether evidence needs to be secured immediately, and whether internal reporting lines are too compromised to manage the matter alone. In more sensitive cases, that outside perspective also helps preserve neutrality and reduce the risk that internal loyalties distort the facts.

There is also a practical business reason to involve outside counsel early. Fraud issues rarely stay confined to the accounting line item where they first appear. They can affect vendor contracts, tax records, insurance questions, employee claims, and future litigation strategy, as discussed in Business Legal Services for Small Businesses in Texas. If senior management delays too long, the business may lose time that cannot be recovered later.

Suspect Misconduct? Contact Kowtun Law for a Confidential Consultation

When the numbers stop making sense, the first goal is not to react loudly. It is to slow the issue down, preserve the right facts, and decide whether the problem is an error, weak controls, or something more serious. A measured response often gives the business better options than a rushed internal accusation.

Kowtun Law focuses on investigative, due diligence, and business legal services, with a clear, actionable, and personally handled approach for business owners dealing with sensitive matters. When financial irregularities raise questions the business cannot answer cleanly on its own, a confidential legal review can help determine the next step before the issue becomes harder to contain.

FAQs

What Is the Difference Between Corporate Fraud and Embezzlement?

Corporate fraud is a broad term for dishonest conduct intended to create unlawful gain or conceal loss inside a business. Embezzlement is more specific. It usually involves someone misusing money or property they were trusted to handle. The terms can overlap, and in many investigations the early facts do not show clearly which label fits best until records are reviewed in more detail.

Should a Business Confront the Suspected Employee Right Away?

Usually not. The first step is often to preserve records, limit unnecessary discussion, and assess the issue quietly. A direct confrontation can alert the person, affect devices or documents, and shape what other employees say later. That does not mean confrontation is never appropriate, but it should usually come after the business understands the evidence it already has.

Can a Business Call Law Enforcement Immediately?

That depends on the facts and the stage of the review. In some cases, immediate reporting may be appropriate. In others, the business first needs enough information to avoid making a rushed accusation based on incomplete records. A careful legal review can help decide whether the issue should stay internal for a short period or move into a criminal reporting process more quickly.

What Records Should Be Preserved First?

The business should focus early on accounting entries, emails, approvals, vendor files, reimbursement records, access logs, bank activity, and any devices or systems tied to the suspected conduct. The exact list varies by case. What matters most is speed and discipline. Once people realize a problem is being reviewed, the risk of deletion, alteration, or informal explanation often goes up.

What if the Suspicion Turns Out To Be Wrong?

That possibility should always be taken seriously. A good investigation protects the business by testing facts, not by forcing a result. If the concern turns out to be error rather than dishonesty, the company still benefits from understanding what failed in the process. Often the result is stronger controls, clearer authority lines, and a more defensible internal response than a rushed accusation would have produced.

Who Should Know About the Investigation Inside the Company?

Usually only a small group should know at the start. That group often includes ownership, selected senior management, and legal counsel depending on the issue. Broad internal discussion creates risk. It can affect witness accounts, damage reputations unnecessarily, and make privilege or confidentiality harder to maintain. A narrow circle also helps the business keep daily operations stable while facts are still being tested.

Can a Fraud Investigation Focus on an Executive or Senior Manager?

Yes. In some cases it must. Seniority does not reduce the need for review, and in many businesses, it raises the stakes because the person may control records, influence employees, or shape the internal response. That is one reason outside counsel is even more critical when leadership is involved. Internal reporting lines may not be reliable enough to handle that issue fairly.

What Should a Business Do After Misconduct Is Confirmed?

The answer depends on the amount at issue, the evidence, the employee’s role, insurance coverage, contractual rights, and whether the conduct may need to be reported outside the company. Some matters call for termination and recovery efforts. Others also involve civil claims or criminal referral. The business should also review control failures so the same weakness does not remain in place after the individual issue is addressed.

Recent Blogs

-

What Business Owners Must Know Before Signing Contracts

-

LLC vs Corporation vs Partnership: How to Choose the Right Business Structure in Texas

-

Independent Contractor vs Employee: What Your Business Contract Must Clearly State

-

How to Handle Employee Complaints the Right Way (Before They Become Lawsuits)

-

Legal Risks of Ignoring Workplace Issues

Peace of Mind for Your Business Decisions

Schedule your confidential consultation today!

© Copyright 2025-26 All Rights Reserved.